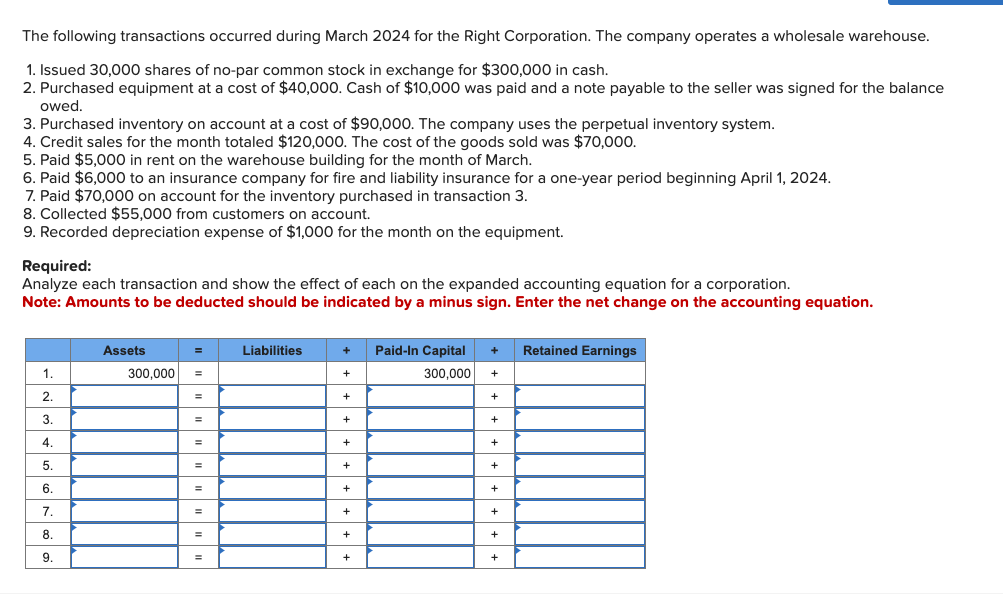

.gif&w=566&h=133&zc=1)

Piggyback mortgage

- A first mortgage, normally to own 90% of your residence’s value

- A house collateral credit line (next mortgage’) worth 10% of the home’s worthy of

With this particular design, the home consumer renders an effective 10% deposit. And also the family guarantee credit line (HELOC) will act as several other 10% downpayment.

So, in place, the new debtor was getting 20% down without in reality being required to save an entire installment loan Fresno OH 20% in dollars.

PMI is recharged of many financing with lower than 20% off, and it also adds an extra month-to-month expenses for the homeowner. To prevent it may save you a couple hundred dollars monthly.

The disadvantage out of a piggyback mortgage would be the fact you take out a few independent lenders at once. So you have two monthly money, each other having attention.

When you find yourself wanting this plan, correspond with that loan officer otherwise mortgage broker who can let determine your repayments and determine whether or not good piggyback mortgage create rescue you currency.

Types of mortgage loans FAQ

The new four fundamental form of mortgage brokers is antique loans, FHA finance, Virtual assistant finance, and USDA loans. Traditional finance commonly backed by the us government, but the majority need certainly to see credit recommendations place by the Federal national mortgage association and you will Freddie Mac computer. FHA, Va, and you can USDA loans are typical supported by the us government but offered by private loan providers. Most top loan providers bring all financial applications, though USDA funds can be a little harder to find.

The preferred kind of mortgage try a normal financial, that is one mortgage not backed by the federal government. This is what many people think about since the a standard’ mortgage. Old-fashioned funds is actually versatile; down money can range out of step 3 so you’re able to 20 percent or higher, and also you only need an excellent 620 credit history so you’re able to be considered with most loan providers. Such financing make up regarding 80 percent of one’s mortgage industry, according to the Freeze Mortgage Tech Origination Declaration.

An informed variety of mortgage hinges on your situation. When you yourself have high borrowing from the bank and you may a 20 percent downpayment, antique loans usually provide the cost effective. If you’d like additional let qualifying on account of all the way down credit scores or earnings, a keen FHA loan will be best. So if you’re a qualifying veteran otherwise armed forces affiliate, a beneficial Va loan is always the best choice. The loan administrator can help you compare loan choices and get ideal financing for your requirements.

Virtual assistant fund routinely have a decreased rates of interest. But not, the brand new Va system is only accessible to eligible provider professionals and experts. To own non-Va consumers with solid borrowing from the bank, a traditional financing tend to typically provide the lower costs.

Having very first-day home buyers which have a 20 percent down-payment and a great credit, a standard old-fashioned financing is often top. If you are searching to possess a minimal down payment, this new Va, USDA, and you can FHA financing programs are all a beneficial possibilities. Virtual assistant and USDA allow it to be zero down-payment to possess eligible people. And you may an FHA loan makes it possible to be considered with a credit score as little as 580.

Yes! The fresh Va financing system, open to pros and you can service members, enables zero advance payment. Very really does the fresh USDA financing program. So you’re able to be considered having USDA, you must pick into the a professional rural area and your family income need to be inside local earnings limitations.

Minimal credit rating to help you be eligible for a home loan try 580, through the FHA financing program. Virtual assistant finance can also allow it to be results as little as 580, but not, Va conditions are different by lender and lots of want to see an excellent score off 620 or even more. Conventional and conforming loans require a score of at least 620, and you may USDA loans usually require 640 or even more. If you’d like a great jumbo loan, you will likely you need a rating more than 700.